If there’s one thing I loathe, it is Dilbertian corporate jibber-jabber. I don’t trust it. Yes – even a completely empty conference room is more productive.

Whenever someone strings lots of fancy sentences together during an estate planning meeting, you can bet they’re either trying to pull a fast one or clouding over the obvious with needless complexity. One thing is certain: it is NOT precise financial thinking. Sadly, investment advice far too often gets suffocated by this type of toxic corporate jibber-jabber.

After many years of experience in different fields, SIMPLE is almost always better (I do mean that – not just in finance– think about your last relationship… Seems fun in the beginning – less so after the reality TV show…)Â

Occam knew what he was doing when he broke out his now historic philosophical razor . . . As with metaphysics, so it goes with investing. The wisest financial principles should be readily apparent. Almost all of the “complicated†investment concepts out there aren’t worth the endless blather necessary to make them salable – let alone profitable. If you can’t advise your client with simplicity, it is improbable that you have what you’ll need to advise them with meaning.

So, with those thoughts as prologue, here is my personal guiding investment principle: Focus on long-term purchasing power. Relentlessly.Â

Purchasing power is having the resources to buy things. And it’s never the function of a single variable.  You always want to have enough purchasing power to buy what you need when you need it. No person or entity has unlimited purchasing power. Hence, merely possessing purchasing power does NOT mean you can always buy (or sell) what you want when you want it.Â

Failing to understand that basic distinction is likely the most destructive trait exhibited by bankers who unfairly tarnish the wealth management profession and, frankly, breach fiduciary duties while doing it. Remember: It’s never enough merely to tell your clients the truth – a real financial manager reminds them about the truth again and again. The words “responsibility†and “occasional†are like sharks and seals – they don’t mix well (at least for the seals)

Baseball analogies most certainly certainly resonate… (Question: Why isn’t A-Rod looking especially happy here?)

The goal for most people is to preserve one’s purchasing power over market cycles and, then, across generations. It is against that backdrop that one should make investment decisions. Short-term success (or failure) doesn’t offer a sufficiently robust sample-size to determine the effectiveness of a particular skill or process. (Think of Kevin Maas from the Yankees who hit it out of the park 10 times during his first 72 at-bats yet ended his career amassing just 65 additional homers) Like all great things, successful skills and processes can erode. (Now, think of Alex Rodriguez . . . an undisputed offensive force . . . until recent circumstances, including age, have made him more pedestrian).

Smart investors (and their advisers) should be constantly and carefully evaluating the quality of their decisions as a function of long-term purchasing power impact. How? WITH SIMPLICITY:Â {1) After taxes are paid; (2) After fees are paid; and (3) After inflation.Â

Why? Taxes, fees and inflation accrue before you can actually spend on yourself. The only dollars that matter are those still sitting on the table after these inevitable costs have been incurred.

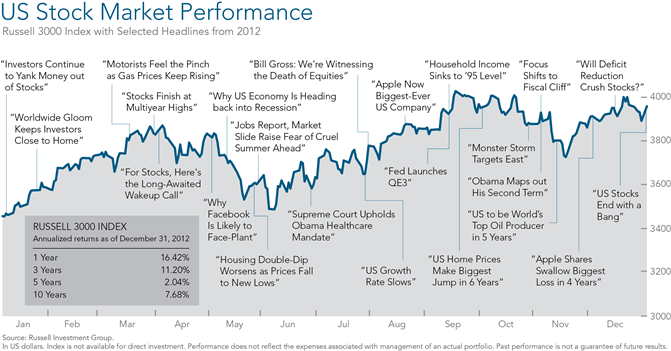

To put it even more bluntly, if your investment performance can’t hold up under this simple benchmark, then it almost surely won’t meet your long-term spending needs.  Over the long haul, everything regresses to the mean.  Markets go up and down. Just look if you don’t believe me . . .

Attempting to time those shifts is a fool’s errand. Â Too many base their investing approach on the functional equivalent of a one-time ludicrously great weekend in Vegas. And what do accidents and Vegas both have in common? They are NEVER demonstrations of repeatable skill. Any adviser who tells you otherwise (outside of Vegas…), isn’t worth your time. Â

Financial advisers who construct long term plans capable of defending your purchasing power against taxes, fees, and inflation are those who will help you (and your bank account) the most. They at least EARN their fees.

Now, blackjack dealers work extremely hard and earn their fees too – BUT FOR VERY DIFFERENT REASONS.